Business Structure: How it Impacts Your Personal Liability

You already know that to start a company, you need to choose a business structure. But how will your choice affect your personal liability?

The fear of your personal assets being on the line for business debts or legal issues can be crippling.

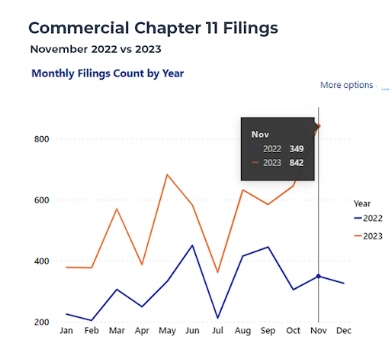

We understand your concerns especially because bankruptcy filings including all chapters increased by 21% from 31,187 in November 2022 to 37,860 in November 2023.

Commercial chapter 11 filings in particular, increased by 141% from 349 in November 2022 to 842 in November 2023.

Image via American Bankruptcy Institute

Fortunately, understanding the complexities of business structures can be the key to overcoming this challenge.

This article will explore the impact of different business structures on your personal liability, helping you make informed decisions.

Let’s get started.

Common Types of Business Structures

Various types of business structures exist, each with its distinct characteristics, advantages, and limitations. Let’s take a look at the most common ones.

Sole Proprietorship

As its name suggests, a sole proprietorship is owned and operated by a single individual. This means that the owner has full control over all business operations and decision-making.

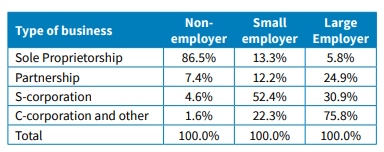

This business structure is the most common. According to SBA, 86.5% of non-employer firms are sole proprietorships.

Image via SBA

Here is what sets a sole proprietorship apart from other business structures:

- Easy to establish – This business structure requires minimal paperwork, formalities, and capital to start.

- Single entity – A sole proprietorship is not a separate legal entity from its owner. The business and the owner are considered as one entity.

- Unlimited legal liability – Since the business and owner are one legal entity, the owner risks losing personal assets to business debts and liabilities. Creditors may seize your vehicle, house, or other belongings to cover your debts.

A sole proprietorship can be an ideal choice if you are starting a low-risk business. It can also be a great way to test your business idea before launching a more formal entity.

Partnership

Partnerships involve two or more individuals sharing business ownership and responsibilities.

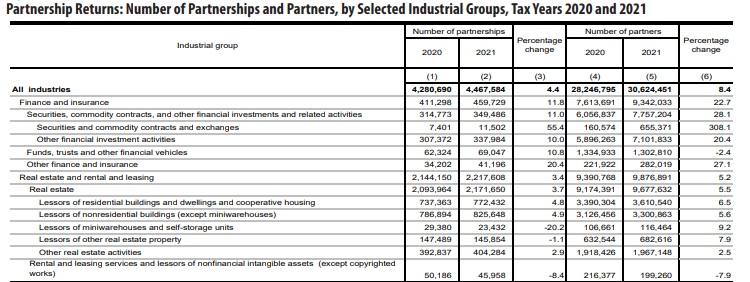

A recent report shows that partnerships increased by 4.4% from about 4.2 million in 2020 to 4.4 million in 2021. Limited Partnerships accounted for 9.9% of all partnerships.

Here is a detailed overview of the number of partnerships and partners in 2020 and 2021.

Image via IRS, Statistics of Income Division, Partnerships, May 2023

Common types of partnerships include:

Limited Partnerships (LPs)

A limited partnership has at least one general partner with unlimited liability and some partners with limited liability. This means that the general partner risks losing personal assets to business debts and obligations.

On the other hand, limited liability partners’ personal assets are protected from the company’s debts and legal obligations. However, the general partner has more control over business operations than limited partners.

Limited Liability Partnerships (LLPs)

Limited liability partnerships offer liability protection to all partners, shielding personal assets from business-related liabilities. While this structure protects partners from business debts, it may not shield them from personal liabilities such as:

- Professional negligence or malpractice

- Unlawful actions

- Contractual obligations

Partners in an LLP are not personally responsible for the negligent acts or misconduct of other partners.

Corporation

A corporation is a unique business structure separate from its owners. This means that the members are not personally liable for the corporation’s actions.

The corporation can own assets, enter into contracts, and pay taxes separately from its owners. What does this mean?

It means that a shareholder can leave the corporation or sell their shares without disrupting business operations.

This business structure exists in various forms:

C Corp

C Corps are the standard corporation structure, offering limited liability to shareholders. Members only risk losing their initial investment and not their personal assets to the corporation’s losses.

One downside of C Corps is that they are taxed twice. Once when the corporation makes a profit, and again when dividends are distributed to shareholders.

S Corp

Like C Corps, S Corps provide limited liability to shareholders, protecting their personal assets.

However, this business structure avoids double taxation by passing shareholders’ profits and some losses through to their personal tax returns. This way, the corporation is taxed only at the individual level.

Nonprofit Corporation

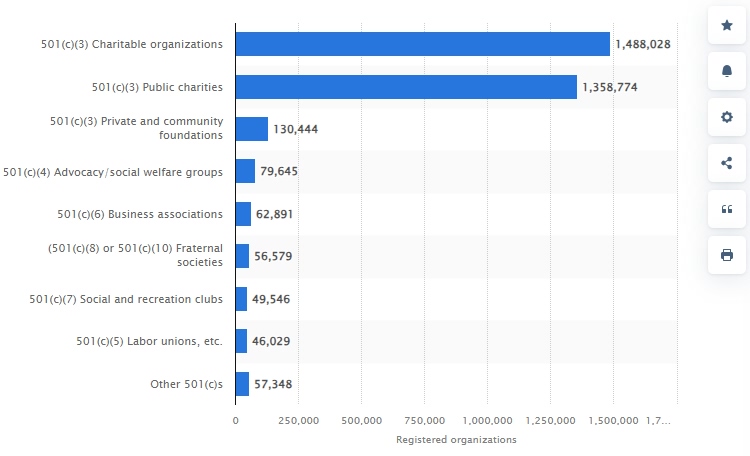

Nonprofit corporations are created for charitable, educational, religious, or other non-profitable purposes. In 2021, the number of charitable organizations in the US reached 1.49 million.

Image via Statista

Non-profit organizations don’t distribute profits to members. Instead, they reinvest surplus funds back into the corporation. Let’s take a look at what makes this business structure unique:

- Liability – Members are protected from personal liability to the organization’s debts and obligations. However, limited liability does not cover intentional personal negligence.

- Tax exemptions – Since these corporations work for public benefits, they are eligible for tax exemption.

Registering a non-profit organization and applying for tax exemption can be complicated.

Fortunately, the GovDocFiling guide can help you fill out a tax ID application to get an EIN tax ID. You only need to carefully follow the right steps to simplify the application process and avoid delays.

Limited Liability Company (LLC)

A Limited Liability Company (LLC) is a hybrid structure that combines elements of both a corporation and a partnership. According to a previous source, Limited Liability Companies accounted for 71.7% of all businesses classified as partnerships.

Let’s take a closer look at the key features of an LLC:

- Separate entity – An LLC is a separate legal entity from its owners. It can enter into contracts, sue and be sued, and own property independently.

- Limited liability – This business structure protects your personal assets from business debts and liabilities.

- Pass-through taxation – The LLC’s profits or losses pass through to the members’ individual tax returns, preventing double taxation.

- Continuity – An LLC can continue operating when a member leaves if there is an agreement to buy, sell, or transfer ownership. If there is no such agreement, some states might require the LLC to be dissolved and recreated again. This aspect is crucial for multi-member LLCs, where the dynamics of ownership can significantly impact business operations. Understanding the legal framework surrounding such entities can be crucial; consider exploring detailed explanations here.

Choosing the Right Business Structure

Would you risk your personal assets for a business? If so, are the benefits worth it? These are some of the factors you should weigh when selecting a business structure.

Carefully weigh the pros and cons of each business structure to make a wise decision.

Wrapping Up

Personal liability is a critical consideration when selecting a business structure. Each structure has its distinct impact on your personal liability.

Sole proprietorships and partnerships offer simplicity but expose you to unlimited personal liability. On the other hand, LLCs and corporations provide protection, shielding your personal assets from most business-related risks.

The key is choosing a business structure that aligns with your risk tolerance, the nature of your business, and your long-term goals.

Author Bio:

Brett Shapiro is a co-owner of GovDocFiling. He had an entrepreneurial spirit since he was young. He started GovDocFiling, a simple resource center that takes care of the mundane, yet critical, formation documentation for any new business entity.

Headshot: