ACH: Understanding for Beginners

1974 was a huge year for electronic transactions. This is because the National Automated Clearing House Association (NACHA) began governing the ACH network that year. Once NACHA started overseeing ACH, this form of electronic processing began to take off. ACH has developed since then and today is easily accessible. In 2021, over 72.6 trillion funds were conducted as ACH payment transactions. This growth comes as an astounding seventeen percent increase of usage of ACH transactions from the year prior.

What is ACH?

ACH, also known as Automated Clearing House, is a computer-based electronic network for processing transactions. Automated clearing house typically focuses on domestic low-value payments that are between participating financial institutions. Automated clearing house is a United States financial network.

ACH is a way to transfer money from one bank account to another without ever using cash, credit cards, or paper checks. It is a strong alternative to the typical payment transactions because they are electronic. Because the payment is electronic, transactions result in faster payment and is more reliable than checks. It is commonly cheaper to process an automated clearing house transfer than a credit card payment or wire transfer.

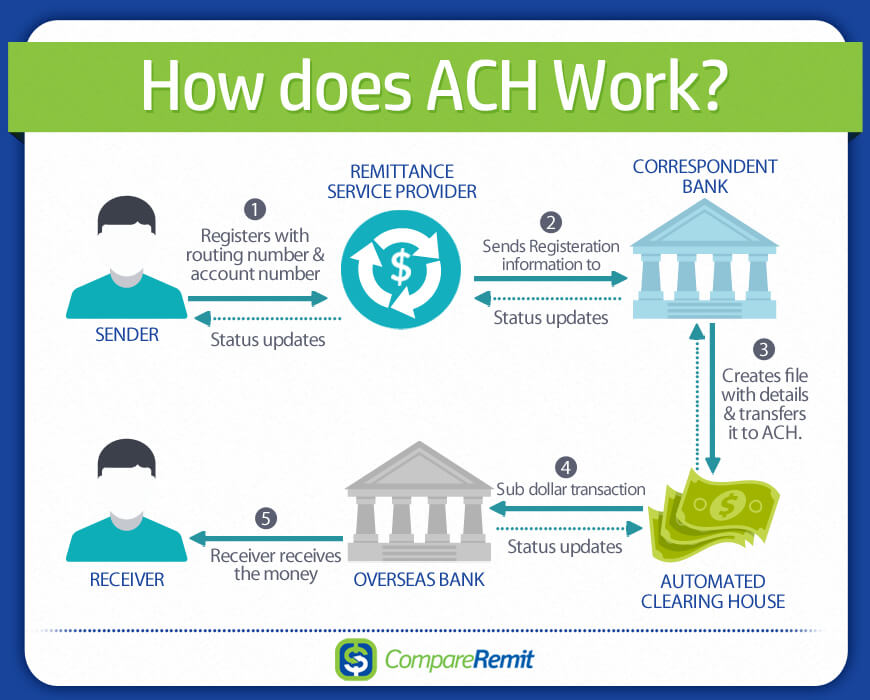

Below is a visual diagram of how ACH functions.

What types of transactions do ACH use?

ACH uses four main transactions:

- Government. The majority of federal payments are used via ACH. This form of a transaction has become a vital part of Americans.

- Consumer. Consumers have the choice to set up recurring payments electronically with a business. ACH gives the business permission to pull directly from the consumer’s account for debit transactions each billing cycle.

- Business-to-Business. Businesses will use ACH to transfer payments electronically. ACH gives businesses the opportunity to make payments for services or request payments for services. This is helpful because businesses don’t need paper checks, cash, or in-person payments.

- International Payments. A global automated clearing house requires the direct deposit of funds into a cross-border bank account through that country’s clearing mechanism. Not all countries have ACH, but use a similar system.

Where ACH is used

Automated clearing house transactions are mainly used in the United States and the nation’s fellow territories. The territories include the U.S Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands. The ACH network is a US-based network, but there are other countries that have recently added automated clearing house processing systems to their usage in the past two years. This includes countries such as Lithuania, Monaco, Andorra, and the Vatican City State.

For countries that currently don’t have ACH, there are alternatives that are quite similar. ACH isn’t used in the UK, Eurozone or other territories. If you are from the European Union you may be familiar with SEPA. Single Euro Payments Area (SEPA) Direct Debit is the EU’s version of ACH. Both are a way to transfer money from one bank to another without using cash, paper checks, or wire transfers.

How ACH can help you

Businesses are competitive and growing with advanced technology each day. Because of this, ACH is becoming increasingly attractive for businesses to use. Here are some reasons why automated clearing house is growing in usage in the business realm:

- Lower transaction fees. Automated clearing house transactions are among, if not the most, cheapest processing fees out of any other form of payment currently. For businesses this can be a huge game changer and savings can be significant.

- Convenience for everyone. Some consumers don’t enjoy using or having credit cards, so ACH is a helpful alternative that provides a faster and more convenient way to manual check payments or wire transfers. Also, additional payment options result in a happier customer experience.

- Less non-payment disputes. ACH is typically less disputed than card transactions, although if you do need to dispute, you can hire an attorney and research your best options.

- Fewer declines due to expiration. Unlike debit or credit cards, bank accounts do not have an expiration date. There won’t be any unnecessary hassle to deal with expiring payment details once processing recurring subscription payments via direct debit.

ACH Focus

There are two main classifications of ACH transactions: direct payments and direct deposits.

Direct payments are local, individual and organization-based. Direct payments focus on the electronic movement of funds to make or receive payments. This form of transaction could be used for sending money to family, paying bills, purchasing a product or service, or supporting a not-for-profit organization.

Direct deposits are administration and business-based. Direct deposits help companies, businesses, and the government with their payments to the consumer. This particularly could be for government benefits, payroll, interest payments, tax refunds, or more. Direct deposits help companies, businesses, and the government with their payments to the consumer.

How Payline can help your business with ACH

If you are curious about getting to know more about ACH, or how it can help your business, Payline data can help. Payline has strong relationship-oriented goals with their clients. Payline is also a transparent company with its customers. Check Payline’s homepage to connect right away with their flexible hours today.

Payline will ensure that your business transactions are quick and easy. This can be seen by their helping over 25,000 businesses this past year with their credit card transactions in the United States, and by consumer’s reviews compared to other competitors they have used prior. Don’t miss out on protecting yourself from identity fraud today.