The Role of Big Data in Fraud Detection and Prevention for Payment Providers

Payment platforms facilitate billions of daily transactions, ranging from eCommerce purchases to digital wallet payments. However, the rise in transaction volumes has also increased the opportunities for fraudsters to exploit vulnerabilities.

With cybercriminals constantly innovating and developing new tactics, traditional fraud detection models have struggled to keep pace, leading to a surge in payment fraud losses. The evidence is clear – payment fraud losses have more than tripled since 2011 and are projected to surpass $40 billion by 2027.

This is where Big Data steps in. It uses advanced analytics and machine learning on vast amounts of transaction data to help payment providers identify patterns and anomalies. But how? Let’s understand in detail! But first, let’s look at how frauds impact businesses.

The Growing Threat of Payment Fraud

Payment fraud is a significant and growing concern for businesses and consumers worldwide. According to a study by Juniper Research, global merchant losses due to online payment fraud will surpass $343 billion between 2023 and 2027. Here are some more statistics that highlight how frauds affect you.

- The number of online banking scams in India nearly doubled in FY23, increasing to 6,659 from 3,596 in FY22. [Source]

- Domestic payments fraud in India increased from ₹542.7 crore in FY 2021 to approximately ₹2,537.35 crore in FY 2023. [Source]

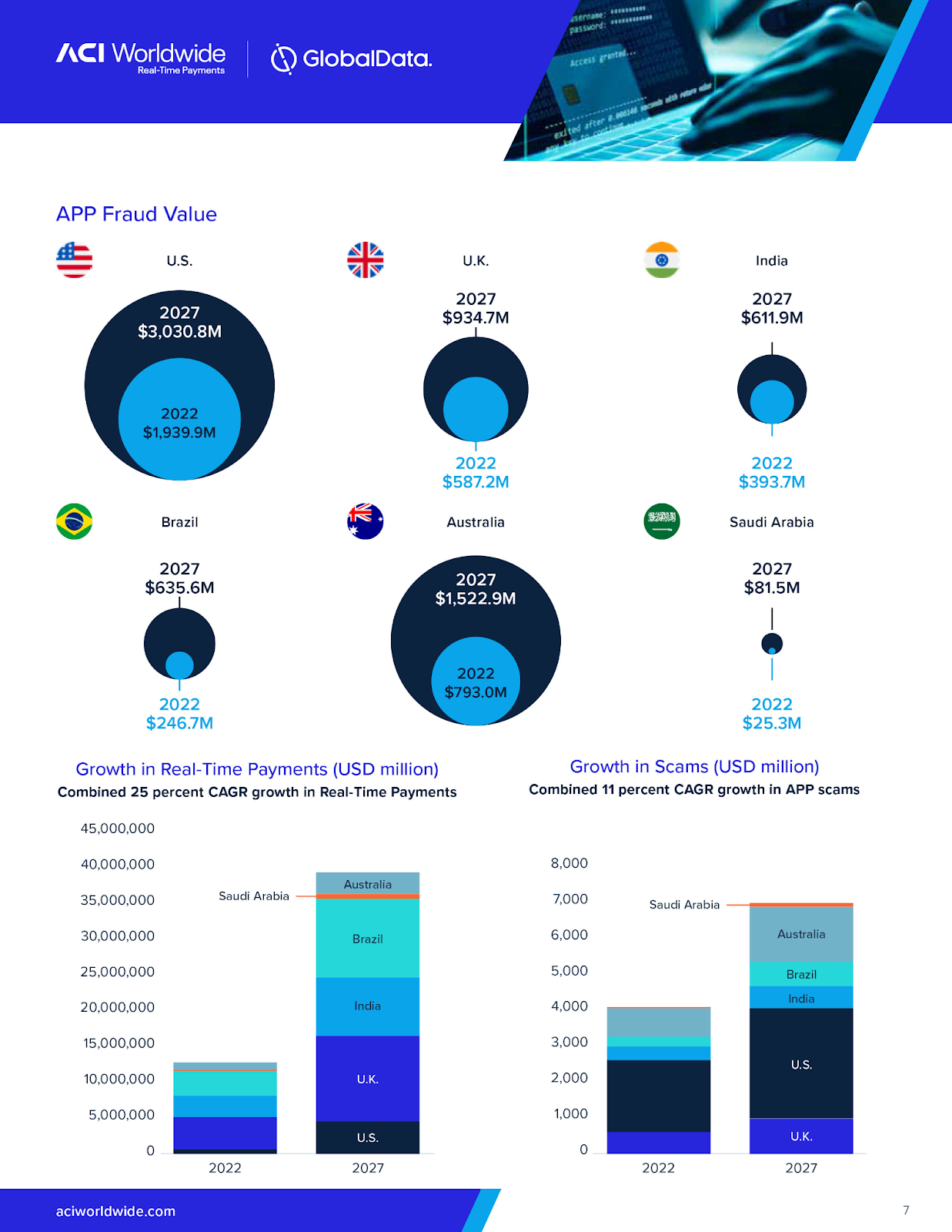

- Authorized push payment (APP) fraud is projected to increase by over 50% in the U.S., reaching over $3.03 billion in 2027, up from $1.94 billion in 2022. [Source]

- Australia is anticipated to have the second-highest amount of APP fraud at $1.5 billion, followed by the U.K. at $934.7 million and Brazil at $635.6 million. [Source]

- 25.5% of scam victims lost over $1,000 in the most recent incident, while 7% of these victims lost more than $10,000. [Source]

These numbers indicate the need for fraud prevention measures. Unfortunately, traditional fraud detection systems are often outpaced by the ever-evolving tactics employed by cybercriminals. One prime example is the rise of Authorized Push Payment (APP) fraud, where fraudsters manipulate victims into authorizing payments through social engineering, phishing, or impersonation. This makes it challenging for conventional systems to detect and prevent such scams. By integrating a robust telecom bss solution, payment providers can enhance their ability to detect and prevent such sophisticated fraud tactics effectively.

(Source)

Understanding Big Data Analytics in Fraud Detection

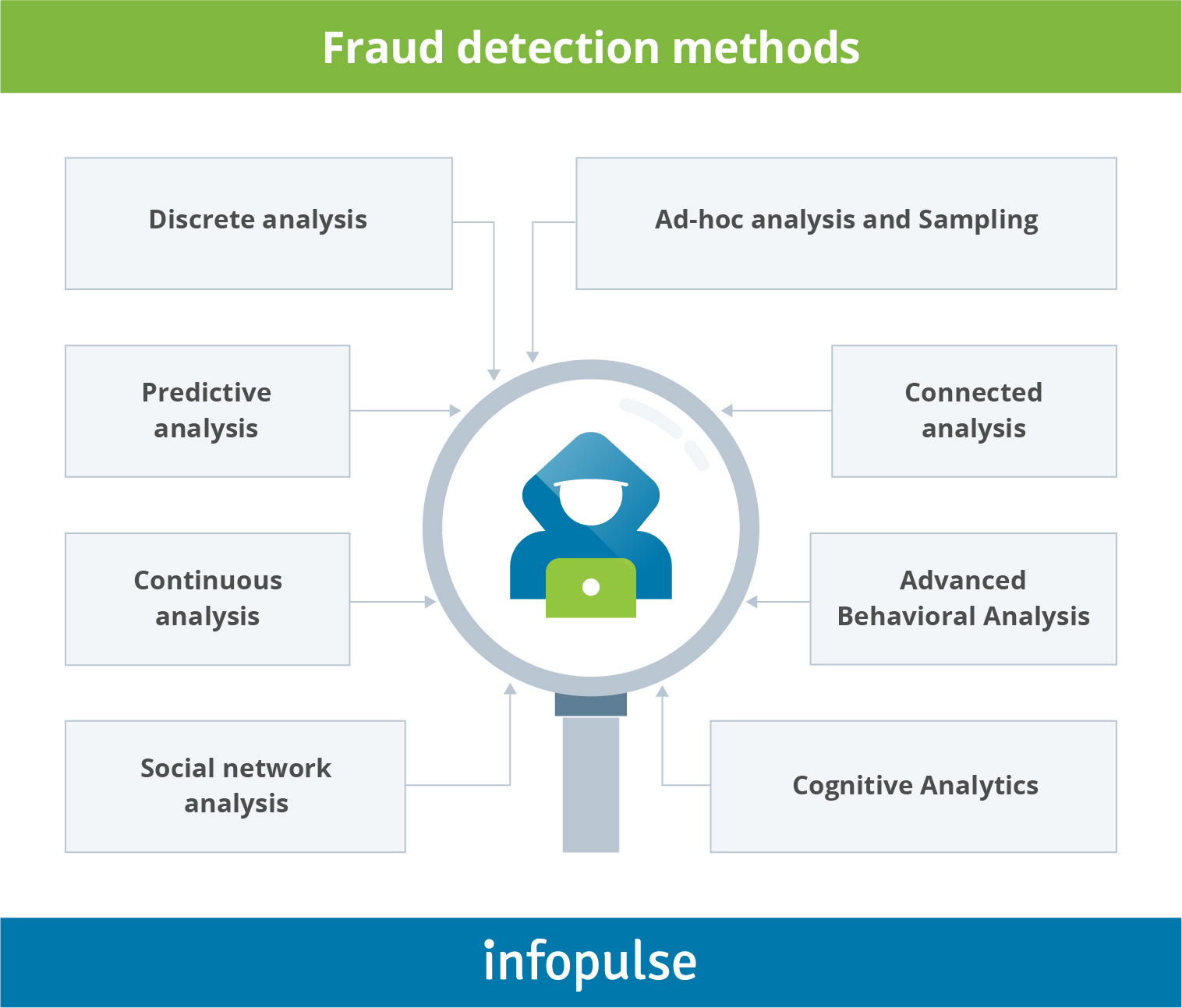

Traditional fraud detection methods use rules-based systems to identify potential fraud. While these methods are effective in detecting known types of fraud, they often struggle to keep up with the rapidly evolving tactics.

On the other hand, big data uses advanced analytical techniques and machine learning algorithms to run background checks by analyzing vast amounts of data. This helps identify patterns and anomalies that may be otherwise difficult to detect. Additionally, big data can learn from new data and evolve.

(Source)

The key components of big data analytics that are particularly relevant to fraud detection include

- Predictive Analytics: Utilizes statistical models and machine learning algorithms to predict the likelihood of fraud by analyzing historical transaction data and identifying patterns associated with fraudulent activities. This approach can be enhanced with Power BI consultancy, offering advanced data visualization and insights to better mitigate fraud risks.

- Anomaly Detection: Employs techniques such as clustering, density-based methods, and outlier detection algorithms to flag transactions that deviate from normal patterns by comparing them to historical data and established baselines.

- Machine Learning Algorithms: Leverages a wide range of machine learning algorithms, including supervised, unsupervised, and deep learning techniques, to learn from data and identify evolving fraud patterns. These algorithms can adapt to new patterns as more data becomes available, enabling continuous improvement in fraud detection capabilities.

Benefits of Big Data in Fraud Prevention

Big Data analytics improves fraud detection accuracy, reduces false positives, and helps personalize customer experiences. Here’s how.

1- Improved Fraud Detection Accuracy

Traditional rules-based systems often miss complex fraud patterns hidden within massive data volumes. Advanced platforms like Frogo.ai leverage machine learning and real-time analytics to enhance fraud detection capabilities by processing multiple data streams simultaneously, identifying sophisticated fraud schemes, and adapting to emerging threats faster than traditional rule-based systems. Big data empowers payment providers to scrutinize diverse data sources like transaction histories, customer behaviors, call analytics, and market intelligence. It can identify intricate correlations and anomalies indicating fraudulent activities. This ensures accurate flagging of suspicious transactions that conventional methods may overlook.

2- Reduced False Positives

Legacy fraud detection systems frequently misclassify legitimate transactions as fraudulent. This not only inconveniences customers but also burdens fraud investigation teams with unnecessary workload. Big data analytics mitigates this by developing a granular understanding of customer behavior patterns. It analyzes a comprehensive range of data points, from purchase histories to device fingerprints, to distinguish genuine activities from potential threats to safeguard online payments.

3- Personalized Fraud Detection

Rather than relying on generalized rules, big data analytics tailors fraud detection models to individual customers. By incorporating data on purchasing patterns, location histories, and channel preferences, it can adapt detection logic to each user’s unique behavioral norms. This personalized approach minimizes the likelihood of erroneously flagging authentic transactions, delivering a more accurate and frictionless experience.

4- Enhanced Customer Experience

Big data analytics enables a hassle-free user experience for customers by reducing the friction caused by unnecessary fraud alerts or declined transactions. Furthermore, big data analytics helps you understand intricate customer preferences, behaviors, and needs. These insights help offer personalized services and finely-tuned recommendations to customers at the right time. A data engineering company can play a crucial role in helping businesses integrate these advanced big data analytics solutions to enhance fraud detection capabilities and overall operational efficiency. For instance, banks can suggest tailored financial products aligned with unique spending habits, investment preferences, or significant life events.

Challenges in Implementing Big Data Analytics for Fraud Prevention

Just like any other technology, big data analytics also comes with its own set of challenges. From privacy concerns to the need for skilled analysts, you’ll likely face these four challenges.

1- Privacy Concerns

Fraud detection strategies analyze sensitive personal and financial data, raising privacy concerns. Strict data governance and strong security controls like encryption, access management, and anonymization techniques are crucial to safeguard customer information. These data governance techniques also help comply with data protection regulations like GDPR, mitigating the chances of penalties or reputation damage.

2- Data Integrity

Inaccurate or incomplete data can undermine the effectiveness of big data analytics, leading to flawed insights and ineffective fraud detection. Payment providers must invest in stringent data quality processes, including data cleansing, fuzzy matching, validation rules, and anomaly detection mechanisms. This helps ensure reliable and error-free analysis.

3- Need for Skilled Analysts

Extracting meaningful insights from complex data sets requires specialized skills. Payment providers need to invest in hiring and training data analysts, data scientists, and machine learning engineers proficient in advanced analytical techniques, statistics, and programming. They can also invest in mentoring software to facilitate knowledge sharing and accelerate skill development within their data teams. Continuous upskilling is vital to keep up with evolving fraud tactics and technological advancements.

4- Regulatory Compliance

Financial institutions must navigate a complex web of regulations related to data privacy, fraud prevention, and consumer protection. Ensuring compliance with frameworks like PCI DSS, AML, and KYC requires a deep understanding of legal nuances, regular risk assessments, and ongoing monitoring. Dedicated compliance teams and robust governance processes are essential to avoid penalties and reputational damage.

Strategies for Implementing Big Data Analytics

Implementing big data to prevent fraud requires a well-structured strategy. This involves establishing methods for data collection, storage, pattern recognition, and real-time monitoring. Let’s understand in detail.

1- Data Collection and Storage

Effective fraud detection and prevention rely on the ability to collect and store vast amounts of data from various sources. Payment providers must establish a robust big data pipeline to handle the growing volume and variety of data.

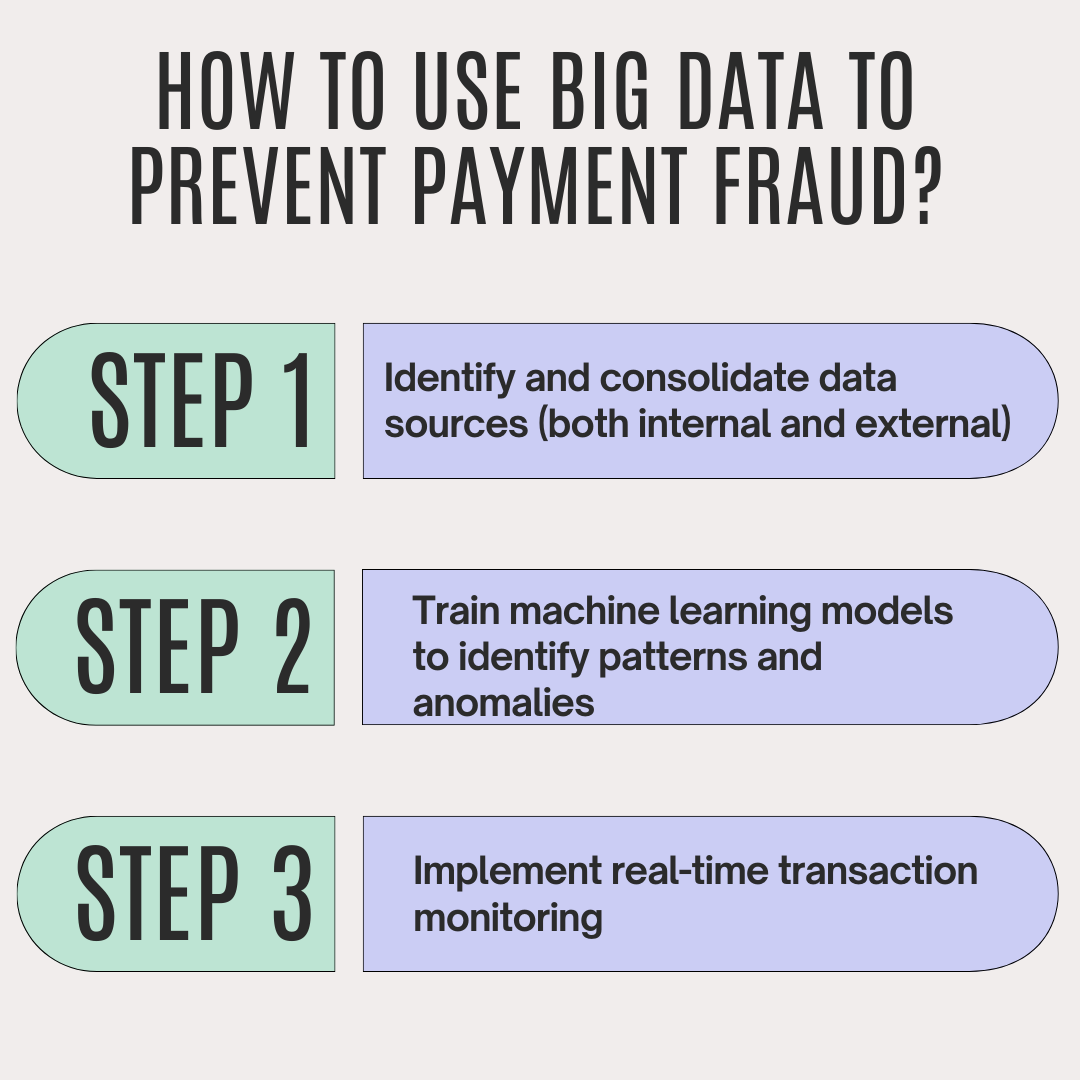

- Identify and consolidate data sources, including transactional data, customer information, device data, and external data sources (e.g., IP addresses, geolocation, social media).

- Implement robust data ingestion pipelines to collect and store structured and unstructured data in a centralized data lake or data warehouse.

- Ensure data quality and integrity through data cleansing, transformation, and validation processes.

- Establish secure and scalable data storage solutions to accommodate the growing volume and variety of data. Using advanced sanctions screening software such as SEON can additionally enhance data analysis capabilities, ensuring comprehensive compliance with regulatory requirements and mitigating risks associated with illicit activities.

2- Pattern Recognition and Analysis

At the core of big data analytics for fraud detection lies the ability to uncover patterns and anomalies within the vast troves of data. Payment providers must leverage advanced analytical techniques and machine learning algorithms to achieve this objective.

- Implement advanced analytics techniques, such as predictive modeling, machine learning algorithms, and artificial intelligence, to analyze the consolidated data.

- Develop and train machine learning models to identify patterns, anomalies, and indicators of potential fraud based on historical data and known fraud scenarios.

- Incorporate unsupervised learning techniques to detect new and evolving fraud patterns that may not be present in historical data.

- Implement effective feature engineering processes to extract relevant features from the data that can aid in fraud detection.

3- Real-time Monitoring and Response

The ability to detect and respond to potential fraud attempts in real time is crucial for payment providers to minimize financial losses and protect their customers.

- Implement a real-time streaming architecture to process and analyze data as it arrives, enabling immediate detection of potential fraud attempts.

- Integrate the trained machine learning models into the real-time processing pipeline to score transactions and flag suspicious activities.

- Establish rules and thresholds for triggering automated responses, such as transaction blocking, account freezing, or alerting fraud investigation teams.

- Develop interactive dashboards and reporting tools and reporting dashboards to visualize fraud detection results, enabling analysts to monitor and investigate potential fraud cases effectively.

- Continuously refine the rules and thresholds based on feedback from fraud investigations and evolving fraud patterns.

Case Studies and Examples

Now that you know how big data helps in fraud detection and prevention, let’s look at how American Express is using big data to do that.

American Express, a $100 billion payments company, leverages vast amounts of transaction data to prevent fraud through advanced machine learning algorithms. These algorithms analyze thousands of data points, such as cardholder information, spending patterns, and merchant details, in real time to identify potential fraud.

It uses enhanced authorization to allow merchants to share additional data (IP addresses, email addresses, shipping details) with American Express. This extra information is cross-referenced against American Express’s data to detect fraud, reducing fraudulent transactions by 60%.

Beyond payment providers like American Express, big data analytics is being leveraged for fraud detection across numerous industries:

Insurance Fraud: Insurers analyze claims data, customer information, social media activity, and third-party data sources to identify patterns and anomalies that may indicate fraudulent claims. This helps detect activities like exaggerated claims, staged accidents, or identity theft.

Healthcare Fraud: Healthcare providers and insurance companies use big data to monitor medical claims, patient records, and billing patterns to detect fraudulent activities such as upcoding, unbundling, or phantom billing. This protects revenue and ensures the proper allocation of healthcare resources.

Telecommunications Fraud: Telecom companies analyze vast amounts of call data records, network logs, and customer information to detect fraudulent activities like subscription fraud, call selling, or theft of services. This helps minimize revenue losses and protect network integrity.

Retail Fraud: Retailers leverage big data analytics on transaction data, loyalty program information, and surveillance footage to identify patterns of return fraud, price arbitrage, and organized retail crime. This safeguards revenue and inventory.

Tax Fraud: Government agencies use big data to analyze tax filings, financial transactions, and third-party data sources to detect tax evasion, underpayment of taxes, or fraudulent claims for deductions or credits.

Cyber Fraud: Financial institutions and enterprises analyze network traffic, user behavior, and threat intelligence data to detect cybersecurity threats like malware, phishing attacks, or unauthorized access attempts, protecting sensitive data and systems.

Conclusion

Payment fraud poses a significant threat to businesses and customers alike. Traditional fraud detection methods are no longer capable of identifying cybercriminals’ latest tactics. Big data, on the other hand, can sift through a vast amount of data, identify patterns, learn from the data, and accurately flag fraudulent transactions. However, ensure that the data you feed is accurate and up-to-date, train machine learning models, and enable real-time monitoring.

Author Bio

Dan Annetts is the director of Outreach + Communication at 800.com. A cloud-based telecommunications provider. With a passion for tech and writing, Dan is often buried in his laptop, keeping ahead of the next trend. When he isn’t working, he’s an avid gym-goer and Tolkien nerd!